The Russian B2B TV Signal Delivery Market: Transition from Satellite to Terrestrial Networks

The Russian market for delivering TV signals to pay-TV operators' networks via terrestrial communication channels grew by nearly 40% in 2023, reaching 960 million rubles. The high growth rate is driven by both global trends — the delivery of «heavy» content worldwide is shifting to terrestrial channels — and the specifics of the Russian market, with its well-developed terrestrial infrastructure. Additionally, artificial interference with satellite resources during the summer and fall of 2023 also contributed to this shift.

Synterra Media, a digital partner in the production, processing, and delivery of media content, analyzed the development of the Russian B2B TV signal delivery market from 2018 to 2023. The study considered data from both open sources and the company's own expert insights.

Participants in the Russian B2B TV Signal Delivery Market

The market for delivering television signals to operator networks can be divided into two main environments:

- Signal distribution via terrestrial communication channels, including non-guaranteed channels (through the Internet);

- Signal delivery via satellite communication channels.

Historically, services for delivering television signals via terrestrial communication channels have been provided by specialized telecom operators such as Synterra Media, CVCS «MSK-IX», RTP Media, Nauka-Svyaz, and others.

In recent years, TV signal delivery over the Internet using the SRT protocol (Secure Reliable Transport — an open-source protocol for video transmission) has been actively developing. The advancement and improvement of Internet delivery protocols have allowed companies like Microimpulse, GlobalNet, Home-AP.TV, and others to enter the terrestrial delivery market. In the summer of 2023, due to artificial interference with satellites, even satellite operators, such as Orion Express, began offering terrestrial delivery services, effectively competing with traditional terrestrial operators.

Additionally, in response to satellite attacks, several TV channels began distributing signals to telecom operators via the SRT protocol, using their own technical resources without relying on external companies.

Satellite TV signal delivery has traditionally been handled by companies such as FSUE «Space Communications» (RSCC), Gazprom Space Systems (GSS), Orion Express, STV, and GeoTelecommunications.

Volume of the Russian B2B TV Signal Delivery Market

For a long time, satellite transmission was the primary channel for delivering TV signals. Its main advantage was the wide geographic coverage provided by signals from spacecraft. However, with the expansion and modernization of terrestrial lines for TV signal transmission, media industry participants increasingly began to consider terrestrial delivery as a viable alternative. At the same time, the content itself became «heavier», with a growing number of TV channels being produced in HD and UHD formats, which raised the demand for higher bandwidth in communication channels.

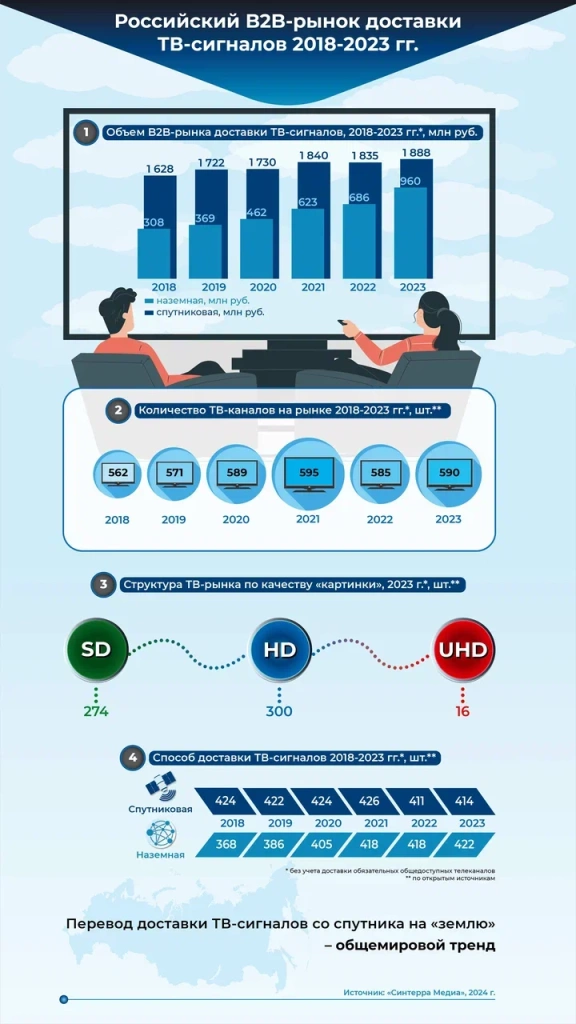

As a result, over the past five years, the Russian TV signal delivery market has grown rapidly. According to Synterra Media experts, in 2018, the volume of the terrestrial delivery market was 308 million rubles, while satellite delivery accounted for 1,628 million rubles. In 2019, the terrestrial delivery segment grew by 19.8%, while satellite delivery increased by 5.7%. In 2020, the terrestrial delivery segment grew even more significantly — by 25.2% (to 462 million rubles), whereas the satellite segment grew by only 0.4% (to 1,730 million rubles). In the post-COVID year of 2021, terrestrial TV signal delivery saw a leap of 34.8%, from 462 million rubles to 623 million rubles, driven by the active development of the «Media Logistics 2.0» project (a joint initiative by Synterra Media and MSK-IX) and the entry of new niche players into the market.

Even in 2022, despite reduced market activity and the exit of several international media players from Russia, the terrestrial TV signal delivery market grew by 10.1%. In 2023, it achieved a record growth of 39.9%. The primary driver of terrestrial delivery growth last year was artificial interference with satellite communication channels by neighboring countries. Broadcasters and operators began to transition en masse to terrestrial communication channels, using satellites as a backup.

«The first incidents of content substitution on TV channels were isolated. However, as hackers realized they could exploit vulnerabilities in satellite signal delivery, the number of cyberattacks increased. Broadcasters were the first to raise the alarm, urging cable TV operators to switch from satellite to terrestrial channels or use satellite as a backup», commented Grigory Uryev, General Director of Synterra Media.

Table 1. Volume of the B2B TV Signal Delivery Market, 2018–2023*, million rubles

| year | terrestrial, million rubles | satellite, million rubles |

|

2018 |

308 |

1628 |

|

2019 |

369 |

1722 |

|

2020 |

462 |

1730 |

|

2021 |

623 |

1840 |

|

2022 |

686 |

1 835 |

|

2023 |

960 |

1888 |

*Excluding the delivery of mandatory free-to-air TV channels

Prerequisites for the Growth of the Russian B2B TV Signal Delivery Market

The rapid growth of the B2B terrestrial TV signal delivery market is primarily driven by the rapid development of Russian terrestrial infrastructure. For instance, in 2023, the construction of Synterra Media's National Media Network, which connected 84 regions, was completed, and the «Media Logistics 2.0» project was launched, featuring more than 200 connection nodes.

In addition, the rapid growth of the Russian terrestrial TV signal delivery market was supported by the development of the media market. The migration of content to terrestrial channels is a global trend driven by increasing consumer demands for TV and Video on Demand (VoD). Content is becoming increasingly «heavy». From 2018 to 2023, the total number of channels in Russia, excluding TV channels included in the first and second multiplexes, grew from 562 to 590. Moreover, in 2022, domestic, Turkish, and Asian channels quickly replaced the products of Western players who exited the Russian market.

Table 2. Number of TV Channels in the Market, 2018–2023*, units**

|

|

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

|

TV Channels |

562 |

571 |

589 |

595 |

585 |

590 |

*Excluding the delivery of mandatory free-to-air TV channels

**Based on open sources

At the same time, the number of HD and UHD channels, which are more demanding on TV signal delivery infrastructure, has increased (transmitting higher-quality images requires a broader channel). For example, at the beginning of 2018, there were approximately 250 HD channels on the Russian market, and by the end of 2023, their number had grown to 308. The number of UHD channels increased from 10 to 16 over the past six years.

Table 3. Structure of the TV Market by Image Quality, 2023*, units**

|

SD |

HD |

UHD |

|

274 |

300 |

16 |

*Excluding the delivery of mandatory free-to-air TV channels

**Based on open sources

In 2018, 424 TV signals were delivered via satellite, while 368 were delivered via terrestrial channels. By the end of 2023, the share of the terrestrial segment had grown, while the satellite segment had declined: 414 TV signals were delivered via satellite, and 422 via terrestrial channels. Moreover, terrestrial delivery is increasingly becoming the primary channel, with satellite delivery serving as a backup.

Table 4. TV Signal Delivery Methods, 2018–2023*, units**

|

|

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

|

Terrestrial |

368 |

386 |

405 |

418 |

418 |

422 |

|

Satellite |

424 |

422 |

424 |

426 |

411 |

414 |

*Excluding the delivery of mandatory free-to-air TV channels

**Based on open sources

Additionally, the high growth rate of the terrestrial TV signal delivery market is explained by Synterra Media experts as being due to the fact that using terrestrial infrastructure is five to six times cheaper for operators than satellite infrastructure. This is especially critical for HD and UHD signals.

Conclusions

The transition of TV signal delivery from satellite to terrestrial channels is a global trend driven by the shift to heavy HD/UHD formats and increased requirements for channel bandwidth.

In Russia, the rapid growth of the terrestrial TV signal delivery market is attributed to:

- A high level of development of terrestrial infrastructure;

- Significantly lower costs of terrestrial delivery compared to satellite;

- Reduced expenses on specialists required for configuring and maintaining satellite equipment;

- Substitution of TV content by cybercriminals and attacks on satellite communication channels;

- Higher levels of security and information protection.

JSC «Synterra Media» is a digital partner in the production, processing, and delivery of media content. The company has developed expertise in servicing key stages of television production and media content distribution: delivery of video content for TV production (contribution), global distribution of TV programs for broadcasters and operators of terrestrial/satellite/cable/IPTV/OTT networks, live event broadcasting, data processing and storage in the «Media Center», as well as the development and implementation of new technologies for the delivery, distribution, and monetization of media content.

Media Contact:

Tatiana Zolotova

PR Partner at Synterra Media

Phone: +7 915 341 48 15

E-mail: zolotovatatiana1@gmail.com

chief@violetviolin.ru

Нажмите для увеличения изображения

{kind=link}